There was a recent Fortune article over the weekend (sorry, it's paywalled) making the ostensibly new case for symbolic (deterministic) reasoning in genAI based use cases to control for hallucinations. It codified some concepts I've been thinking about for some time but didn't yet have the words to describe.

Friendly reminder - artificial intelligence (AI) is a very broad field of computer science focused on enabling machines to perform tasks that typically require human intelligence. Generative AI (genAI) is a more narrow subfield focused on using deep learning and transformer models to generate new content.

You'll have to bear with me through some definitions and an AI history lesson to get to the mortgage point but I promise it will be worth it.

When I first read the article I was thinking "symbolic AI" was a fancy new thing, but really it's been around since the 1950s thanks to Newell and Simon pictured below. It's an early form of artificial intelligence that represented knowledge as symbols and logic. This was the era of rules based so-called "expert" systems. You can think the early days of Desktop Underwriter - given a set of inputs, a deterministic output will be produced. The bottleneck here is acquiring and accurately expressing the logic.

Automated reasoning is the field of computer science that studies how computers can be used to reason logically through a problem. Use the mathematical concepts of proving theorems and solving equations to draw conclusions from a set of rules. (I know, right? Taking me back to me theoretical math days of college, I knew that would come in handy).

Automated reasoning is a big deal because it goes beyond rule-based systems by providing formal, mathematical proofs of correctness, ensuring that results follow logically from the rules rather than relying on rules that may themselves be incomplete or inconsistent. John Alan Robinson came up with this idea in his 1965 work.

Throw in some neural networks to the stew of structured cognitive models and voila - the neuro-symbolic AI field is born. Use symbolic AI to encode the rules, automated reasoning to prove the rules are right, and add a neural network to gobble up all the data and learn. Yowza.

Modern mathematics is more about groups of collaborators working together, rather than any one or two mathematicians making breakthroughs. I selected Josh Tenenbaum as our final mathematician for the article because of his contribution to neuro-symbolic AI and this amazing photo.

I promise I have a point. We all know that hallucinations (also called confabulations) are the achilles heel of genAI solutions in mortgage. I often get the question "how do you know it's right?" and, in fact, I have a dedicated evals team that is solely focused on content errors analysis, prompt (re)engineering and system evaluations. All they do is study data and genAI system behavior to answer this question and prove it.

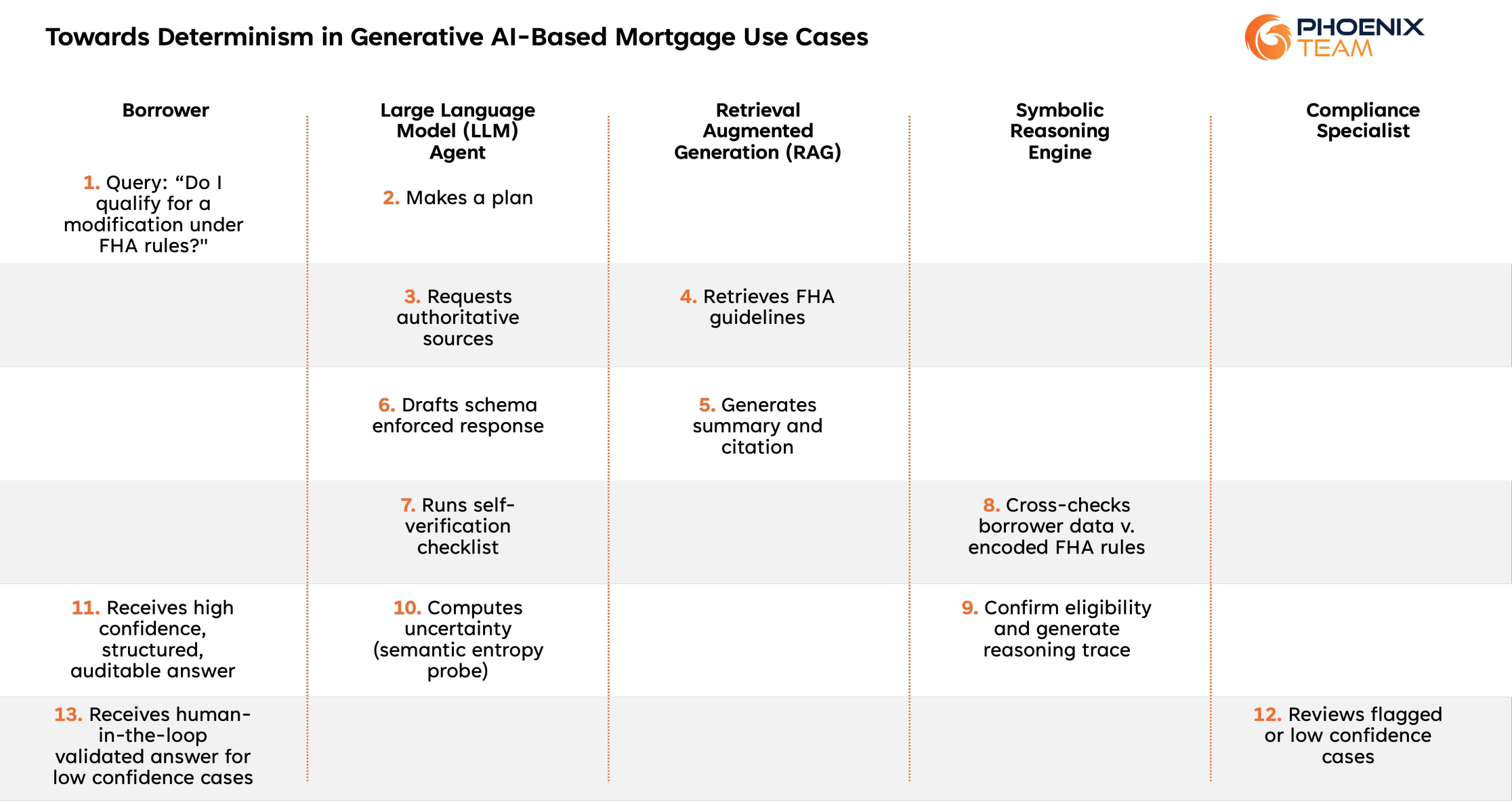

Let's consider the addition of deterministic functions on the typical agentic mortgage flow as in our next diagram. We use the basics of an agent to make a plan and delegate tasks, and we introduce multiple techniques to control for hallucinations. In step (6) we enforce format through a schema - the first control point after prompt engineering. In step (8) we introduce a deterministic rule check confirming eligibility and generate the reasoning trace. Then in step (10) a subagent computes uncertainty using a semantic entropy probe (fancy name for hallucination detector). Finally, we can send high confidence results directly to the borrower, and send low confidence results to a human-in-the-loop (HITL).

Seems legit, right? Why don't we do this all the time?

The main problem I have with this is that it's very expensive and not very fast. I mean why not just code it deterministically the first time? The borrower has what they feel is a simple question, and here we are taking 13 steps through at least four solutions to give them an answer. Not a great customer experience.

Well deterministic decisioning is what got us into this problem in the first place. We have all these ancient, rules-based systems that are literally collapsing under the weight of regulatory change. Yes, it's more overhead to do it this way, but in theory it would allow us to perfect our agentic experiences, learn additionally from error and confidence analysis, and ultimately achieve highly trustworthy generative solutions that are more dynamic and (ultimately) less expensive to maintain. That's my theory anyway.

In this way, we combine probabilistic and deterministic solutions to our use cases to vastly reduce hallucinations. We tradeoff speed and cost, however, which we all know will be hard to overcome in the financial climate of mortgage. I'm just not sure the money is there to go this way. Time will tell, we'll work it in the lab, of course, and keep you posted.

By Tela G. Mathias, Chief Nerd and Mad Scientist at PhoenixTeam, CEO at Phoenix Burst